So, what are USDA loan income limits? Think of them as the guardrails the U.S. Department of Agriculture puts in place to make sure its zero-down-payment home loan program gets to the people who need it most—low- to moderate-income families.

These limits aren't some one-size-fits-all national number. They change quite a bit depending on where you live and how many people are in your household. Getting a handle on your local limit is the first critical step you'll take on your homebuying journey.

Understanding USDA Loan Income Limits

The whole point of the USDA loan program is to boost homeownership in rural and suburban communities across America. To hit that target, the program has to focus on homebuyers who could really use the help. That’s exactly where USDA loan income limits come into the picture. They act as a gatekeeper, ensuring the program's incredible benefits—like no down payment and great interest rates—are reserved for the right audience.

Basically, these limits set the maximum gross household income a family can bring in and still get the green light for the loan. The USDA adjusts these numbers to match the local cost of living, which is why you'll see different limits from one county to the next. It just makes sense: a pricier area will have a higher income cap than a more affordable one.

How Household Size Affects Limits

Where you live is only half the equation; your household size is just as important. The USDA gets that bigger families have bigger expenses, so they adjust the income limits to match.

For the most part, households fall into two groups:

- 1-4 members: This group gets the standard, or baseline, income limit for that county.

- 5-8 members: This group gets a higher income threshold to account for the larger family size.

This tiered approach keeps things fair and accessible. For example, the baseline USDA income limits for 2025 are $119,850 for a household of 1-4 people and $158,250 for a household of 5-8 people in most parts of the country. These numbers went up from last year to keep pace with rising median incomes. You can discover more insights about these updated USDA limits and what they mean for homebuyers.

Trying to figure all this out on your own can feel like a lot, but you don't have to. An expert at Residential Acceptance Corporation (RAC Mortgage) can walk you through the specific limit for your area and family size, clearing the path forward.

One thing to remember: the USDA looks at your total household income, not just the income of the person applying for the loan. This means the gross income of every adult who will be living in the home gets counted.

Nailing down these basics is your first real step toward that zero-down-payment home loan and making your homeownership dream a reality.

How USDA Calculates Income Limits for Your Area

Ever wonder where the USDA gets its income numbers from? They aren't just pulled out of a hat. The limits are carefully calculated to reflect what's actually happening financially in your specific community. This ensures the program helps the people it's meant to help, right where they live.

The whole system is built on a key piece of local data: the Area Median Income (AMI). Think of AMI as the financial center point for your county. If you lined up every household's income from lowest to highest, the AMI is the number smack in the middle—half earn more, and half earn less. The USDA uses this as the starting block to figure out what "moderate income" looks like in your neck of the woods.

The Core Calculation Explained

Once the USDA has the AMI for a county, the math is pretty straightforward. For most places, the income limit for a household of one to four people is set at 115% of the AMI. This percentage is the sweet spot—it’s high enough to be realistic for working families but keeps the program focused on its mission.

This is what makes the program so fair and effective across the country. An area with a higher cost of living will naturally have a higher AMI, which means the USDA income limit will be higher, too. It’s an adaptable system that makes sense.

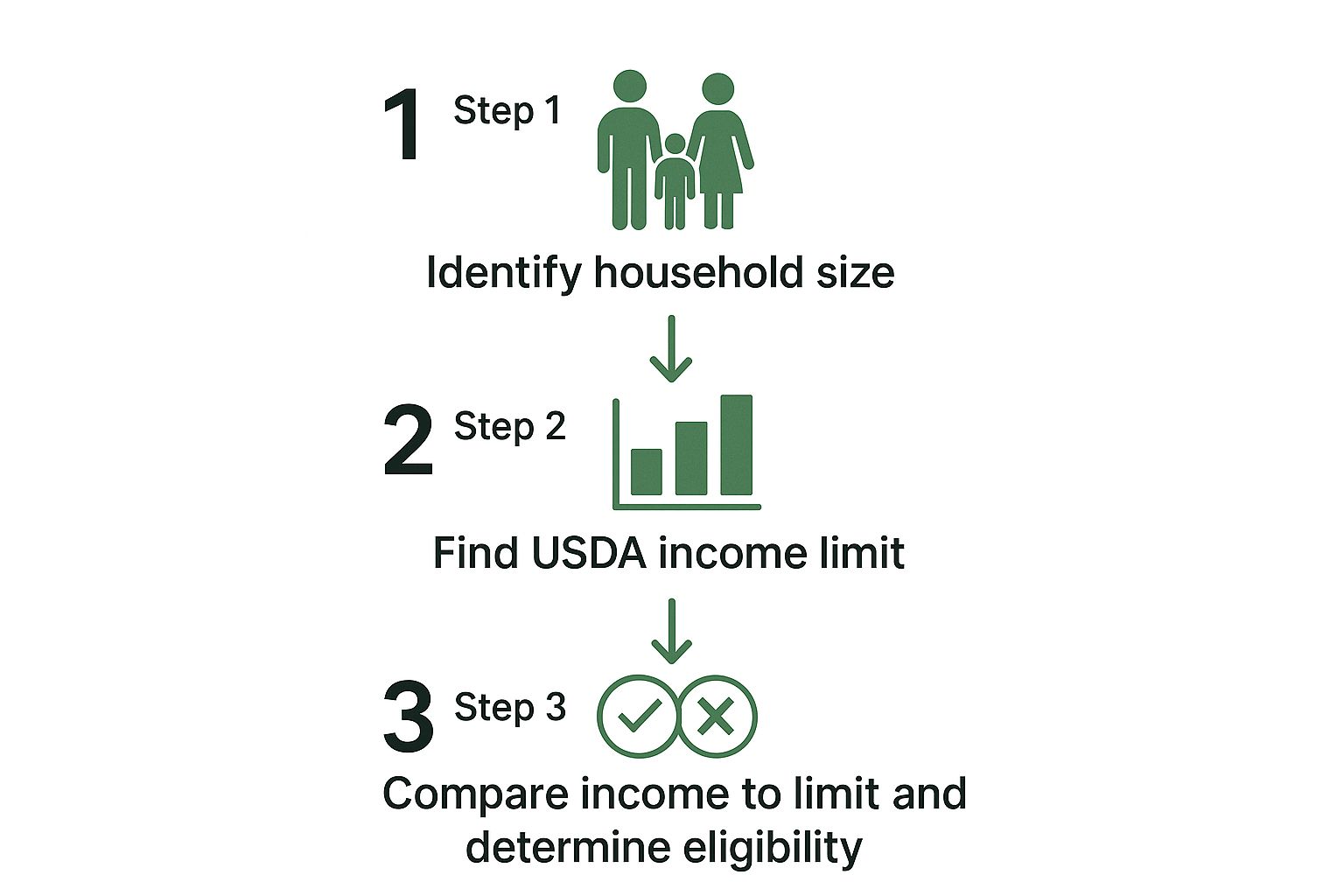

The infographic below breaks down the simple steps to see where you stand.

As you can see, it really comes down to three things: knowing your household size, finding the limit for that size in your county, and comparing it to your income.

Adjusting for Household Size and Location

The USDA doesn't stop with a single baseline number. They dig deeper, partnering with the Department of Housing and Urban Development (HUD) to get fresh AMI data every year for every county and rural area.

After they set that 115% baseline for households of 1-4 people, they make adjustments for bigger families. It costs more to raise more people, right? So, households with five or more members get a higher income cap to account for that, often bumping the limit up to anywhere from 132% to 140% of the area's median income. You can explore more about how these adjustments work to see how these rules play out in different regions.

By tying income limits directly to local median income and household size, the USDA ensures its loan program remains a powerful tool for boosting homeownership where it's needed most.

When you understand the logic, you see the limits not as a barrier, but as part of a fair system. If you have questions about the specific AMI in your area or how your household size affects your limit, the experts at Residential Acceptance Corporation (RAC Mortgage) can give you the clear answers you need.

What Income Does the USDA Actually Count?

When you first hear "income limits," it's easy to assume it just means your paycheck. But with USDA loans, the term "household income" is much broader, and it’s a common point of confusion for homebuyers. The USDA looks at the total gross income of every single adult who will be living in the home, even if their name isn't on the loan application.

This comprehensive approach is how the program ensures it serves the families who genuinely fall into that low-to-moderate income bracket. It's not just about what the loan applicant earns; it's about the complete financial picture of the entire household.

Think about a multi-generational family living together. The main applicant, their spouse, a working adult child, and a grandparent receiving social security all chip in. The USDA will tally up the gross income from all four of them to measure against the county's limit.

What Gets Included in Your Household Income

The USDA considers a wide range of income sources to get an accurate financial snapshot. This goes far beyond what you bring home from your 9-to-5.

Here are some of the most common types of income that get counted:

- Wages and Salaries: This includes everything from your base pay to overtime, bonuses, and commissions.

- Self-Employment Income: Net income from your business or any freelance work is definitely on the list.

- Alimony and Child Support: Regular payments you receive are counted as income.

- Social Security and Disability Benefits: These are seen as stable, reliable sources of income.

- Retirement and Pension Income: Any regular distributions from these accounts are included in the calculation.

This total is your gross household income, which is the starting number used to see if you meet the USDA loan income limits for your area.

Understanding your gross household income is the critical first step, but it’s not the end of the story. The USDA also allows for specific deductions that can lower your final number, potentially helping you qualify even if you’re slightly over the initial limit.

Allowable Deductions That Can Help You Qualify

This is where working with a truly knowledgeable lender pays dividends. Certain household expenses can actually be subtracted from your gross income to calculate your "adjusted" income—and that's the number the USDA ultimately uses. The team at Residential Acceptance Corporation (RAC Mortgage) can help you pinpoint every single deduction you might be eligible for.

Some of the most common allowable deductions include:

- Childcare Expenses: For any children in the home aged 12 and under.

- Disability Assistance: Costs associated with caring for a household member who has a disability.

- Medical Expenses for Elderly Members: Certain out-of-pocket medical costs for household members aged 62 or older.

These deductions can make a world of difference. It's also important to remember that while income limits are a key factor, lenders also look at your overall ability to manage your monthly payments. For a deeper dive, check out our guide on what a debt-to-income ratio is and see why it matters so much for your loan approval.

How to Find the USDA Income Limits for Your County

Alright, now that you've got the hang of what goes into the USDA loan income limits, let’s get to the most important part: finding the actual numbers for your county. The good news is the USDA makes this pretty simple with its official eligibility website. Think of this tool as your direct line to the most accurate, up-to-the-minute information.

I know, navigating a government website can feel a little clunky sometimes. But this one is built to give you a clear "yes" or "no" answer without a lot of hassle. You’ll just need a couple of key details to get started—mainly the state and county you’re looking to buy in and your total household income before taxes.

Using the Official USDA Eligibility Tool

The USDA’s Income Eligibility site is the one and only source you should trust for this. It cuts through all the guesswork and gives you the exact thresholds you need to meet.

Here’s a quick step-by-step on how to use it:

- Head over to the USDA’s income eligibility page.

- Pick the state and county where you want to buy a home.

- Type in your total gross household income (that’s the pre-tax income for all adults in the home).

- Enter the number of people living in the household.

Just like that, the tool will tell you if your income is a match for that area.

This screenshot shows you exactly what you'll see on the main page.

As you can tell, the form is clean and simple. It just asks for the basic details it needs to give you a fast assessment.

A Practical Example of Finding Your Limit

Let’s walk through a real-world scenario. Imagine a family of four is hoping to buy a home in a specific county. They would just pop over to the website, select their state and county, enter their total household income, and put "4" for the number of members.

The results page will spit out two key numbers:

- Low Income Limit: This number is for the USDA Direct Loan program.

- Moderate Income Limit: This is the one you’re looking for. It applies to the much more common USDA Guaranteed Loan program.

For our family of four, the site will show the "Moderate Income Limit" for a 1-4 person household in their chosen county. If their gross income is at or below that number, they’ve just cleared the first major hurdle in the process.

Finding your specific income limit is an empowering first step. Once you have this number, you’re no longer guessing—you have a concrete piece of information to move forward with.

With this number in hand, your best next move is to talk to an expert at Residential Acceptance Corporation (RAC Mortgage). We can double-check your numbers, help you find any income deductions you might qualify for, and walk you through the next steps of getting pre-approved.

How USDA Loans Compare to Other Mortgages

To really get why USDA loans are designed the way they are, it helps to put them side-by-side with other big government-backed mortgages, like VA and FHA loans. Each program was built for a different type of homebuyer, and seeing those differences makes it crystal clear why USDA loan income limits are such a core part of the program.

The biggest things that set USDA loans apart are their focus on location and household income. The entire loan is built around strict income caps to help families with low to moderate earnings buy homes in rural and suburban areas. That's a very different mission from other loan programs.

USDA Loans vs VA Loans

When you look at a USDA loan next to a VA loan, the contrast is night and day. VA loans are an earned benefit for military service members and veterans. Because of that, eligibility is based on your service history, not your paycheck.

In fact, VA loans have no income limits whatsoever. This makes perfect sense when you think about it—it's a program meant to thank veterans for their service, no matter what their current financial situation looks like. A USDA loan, on the other hand, is specifically targeted to help a certain income bracket.

USDA Loans vs FHA Loans

FHA loans are another go-to option, especially for first-time buyers, but they play by a different set of rules. While they are known for being more forgiving on credit scores, they do require a down payment, usually 3.5%.

FHA loans also don't have income caps. Instead, they limit how much you can borrow based on county-specific loan limits.

One of the biggest financial advantages of a USDA loan over an FHA loan is its more affordable mortgage insurance. Both the upfront and annual fees for USDA loans are typically lower, resulting in a smaller monthly payment.

For a family that qualifies, that single difference can add up to thousands of dollars in savings over the life of the loan.

To give you a clearer picture, here’s a quick breakdown of how these three major government-backed loans compare.

USDA vs Other Government Loans at a Glance

| Feature | USDA Loan | VA Loan | FHA Loan |

|---|---|---|---|

| Down Payment | 0% required | 0% required | 3.5% minimum |

| Income Limits | Yes, based on county and household size | No income limits | No income limits |

| Location Rules | Must be in an eligible rural/suburban area | No location restrictions | No location restrictions |

| Primary User | Low-to-moderate income buyers | Eligible veterans & service members | First-time buyers, buyers with lower credit |

| Mortgage Insurance | Yes (Guarantee Fee) | No (Funding Fee, often waived) | Yes (MIP) |

This table really shows how the USDA loan carves out its own niche. It’s all about creating a pathway to homeownership for those who might not have a down payment saved up and live within specific income brackets in designated areas.

The specialists at Residential Acceptance Corporation (RAC Mortgage) can run the numbers for you, showing a clear comparison based on your specific situation. If you meet the income and location requirements, a USDA loan often emerges as the more affordable path to homeownership. To take the next step, learn more about how to get preapproved today.

Common Questions About USDA Income Limits

Even after you get the hang of how USDA loan income limits work, you're bound to have questions when you start applying the rules to your own life. That’s a totally normal part of the process, and getting straight answers is the best way to feel confident about moving forward.

This is where we tackle the most common questions homebuyers ask, with direct and practical answers. We'll dig into what happens if your income is just over the line, how different kinds of income are handled, and what other financial pieces need to fall into place.

What Happens If My Income Is Slightly Over the USDA Limit?

This happens all the time. You look up the income limit for your county and realize your household’s gross income is just a hair too high. Don't give up just yet! This is where the USDA’s allowable deductions can be a real game-changer.

The USDA gets that gross income doesn't paint the whole picture of your finances. They allow you to subtract certain expenses from your total income to arrive at an "adjusted" income figure. If that adjusted number slides in under the limit, you could still be good to go.

An experienced mortgage professional is your secret weapon for finding these critical deductions. They know exactly what the USDA is looking for and can help you calculate your adjusted income with precision, potentially turning a "no" into a "yes."

Some of the most common deductions include:

- Childcare Costs: Got kids 12 or younger? You can deduct documented childcare expenses.

- Care for Dependents with Disabilities: Expenses for caring for a child or adult household member with a disability can often be deducted.

- Medical Expenses for Elderly Members: If a household member is 62 or older, certain medical costs can help lower your adjusted income.

An expert at Residential Acceptance Corporation (RAC Mortgage) can walk you through your finances to make sure you're claiming every possible deduction.

Does a College Student's Income Count Towards the Limit?

Great question, especially for families with students living at home. The answer really boils down to one thing: their enrollment status.

As a general rule, income earned by a full-time student is not counted toward the household's total for USDA loan purposes. But if that student is only enrolled part-time, or if they're an adult living in the home who isn't a student, their income will most likely be included in the household total.

Having the right paperwork, like proof of full-time enrollment from the school, is crucial here. The USDA wants to see an accurate picture of the household's stable income, and this rule helps them do that fairly.

Can I Get a USDA Loan If I Am Self-Employed?

Yes, absolutely. Being self-employed doesn’t lock you out of a USDA loan. Plenty of entrepreneurs and freelancers use this program to buy their homes.

The main difference is that documenting your income is a bit more involved than it is for someone with a W-2 job. Lenders need to see a stable and reliable income history, which means you'll need to provide a more detailed look at your financials.

You should be ready to hand over:

- Two Years of Tax Returns: This means everything, including schedules like Schedule C, to show your business's profit and loss over time.

- Year-to-Date Profit and Loss Statement: This gives a snapshot of your current business performance.

- Business Bank Statements: These help verify the income you're reporting matches what's coming in.

A loan officer will typically average your net income from the past two years to figure out your qualifying income. Because there are a few extra hoops to jump through, working with a specialist at Residential Acceptance Corporation (RAC Mortgage) is a smart move. They're used to handling self-employment income and can make the documentation process a whole lot smoother.

Are Income Limits the Only Financial Requirement?

Nope. Meeting the USDA loan income limits is just the first financial checkpoint. Think of it as getting your foot in the door. Once you’re in, you still have to show you have the financial stability to manage a mortgage.

Beyond the income cap, lenders are also going to look at:

- Sufficient and Stable Income: You have to prove you have enough reliable income to comfortably cover the monthly mortgage payments on top of your other debts.

- Debt-to-Income (DTI) Ratio: This ratio measures how much of your monthly income is already spoken for by debt. A lower DTI shows lenders you aren't overextended.

- Credit History: The USDA doesn’t set a hard minimum score, but most lenders, including Residential Acceptance Corporation (RAC Mortgage), are generally looking for a credit score of 640 or higher. A solid history of paying bills on time is key.

Many homebuyers who qualify for a USDA loan find they are also eligible for other types of financial help. It's worth exploring different down payment assistance programs that can help with closing costs and make buying a home even more affordable.

Ready to see if a USDA loan is the right fit for you? The team at Residential Acceptance Corporation is here to provide clear answers and expert guidance every step of the way. Contact us today to start your journey to homeownership.