If you earn a non-traditional salary, the key to buying a home is finding a Tampa mortgage lender for unique income who actually gets your financial situation. Here at Residential Acceptance Corporation (RAC Mortgage), we live and breathe this stuff. We specialize in helping freelancers, gig workers, and business owners get the financing they need to plant their roots in Tampa's vibrant market.

Your Path to a Mortgage with Unique Income in Tampa

Trying to navigate the home loan process with income from freelance gigs, a side hustle, or your own business can feel like an uphill battle. Let's be honest, many traditional lenders just don't know what to do when they don't see a standard W-2. But your hard work and success shouldn't be a roadblock.

This guide is here to clear the fog. We'll show you that homeownership is completely within reach by breaking down:

- What lenders actually mean by "unique income"

- How to document your earnings the right way

- Why working with a specialized lender is your biggest advantage

The goal is to prove that your non-traditional income isn't a liability—it's a strong foundation for buying a home, even in Tampa's hot market.

Facing Tampa's Competitive Market

The Tampa housing market is no joke. It's fast-paced and competitive, which adds another layer of complexity if you're a unique income earner. In fact, it's currently ranked as the 10th hottest market in the nation, with a median home sale price hovering around $375,947.

Strong buyer demand means homes are flying off the market—often in just 29 days. On top of that, nearly 19% of homes are selling for more than the asking price. In an environment like this, having a lender who can confidently vouch for your financial strength is absolutely critical.

To get a better handle on the entire homeownership journey, it's a good idea to review the essential steps of buying a house, which offers solid insights that apply to your situation, too. At RAC Mortgage, we're built to understand the complete picture of your finances and set you up for success.

What Lenders Actually Consider “Unique Income”

When you hear a lender talk about “unique income,” they’re not questioning if your money is real. They’re simply saying your earnings don’t come from a standard, bi-weekly W-2 paycheck. It’s income that requires a slightly different approach to verify because it doesn't follow a predictable, clockwork schedule.

Think of it this way: a typical salary is like a steady, slow-moving river. It’s consistent and easy to measure. Unique income, on the other hand, can be more like a series of powerful waves. It might come in surges—like a freelance designer with fluctuating monthly invoices or a seasonal business owner whose profits are packed into a few key months—but it's just as substantial over time.

The real job for a Tampa mortgage lender for unique income isn't to doubt your earnings, but to document its stability and consistency over a long enough period to prove it's reliable.

How We Translate Your Success for Underwriters

Traditional lenders often hit a wall when they can’t just check a simple W-2 box. Their process is built around a specific type of documentation that most successful entrepreneurs, gig workers, and independent contractors simply don’t have. This is exactly where a specialist like RAC Mortgage steps in to change the conversation.

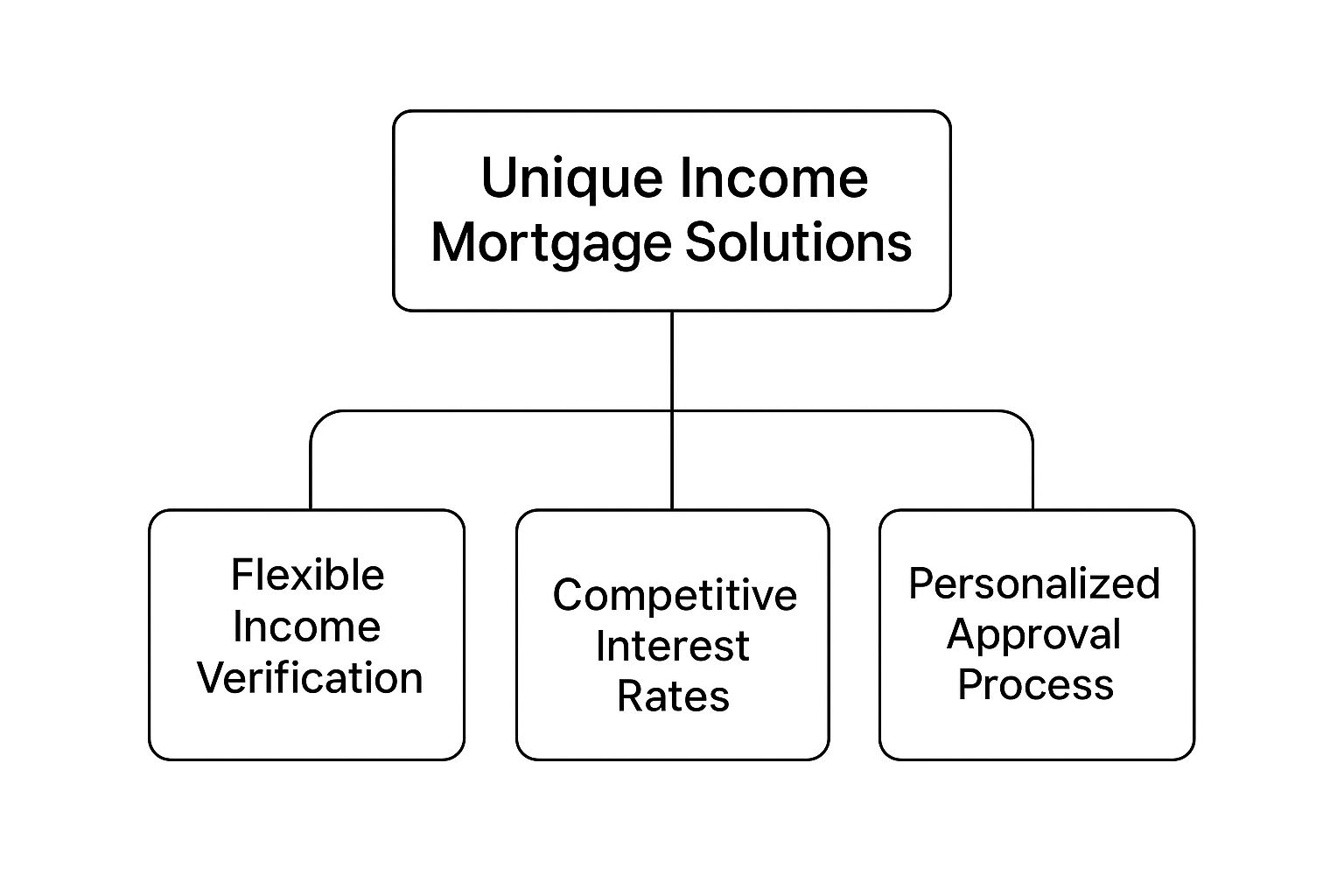

We’ve built our entire process around understanding and documenting these unique financial situations, as you can see here:

This highlights how we combine a personalized approval process with flexible verification methods. It’s not about trying to fit a square peg into a round hole; it’s about building a case that tells the true story of your financial strength. We work to paint a complete picture of your success, not just focus on one small, out-of-context piece of it.

Common Types of Unique Income and Key Documents

To get a mortgage, it all comes down to the paperwork. Lenders need a clear, consistent story of your earnings. Here’s a quick look at some common types of unique income we see and the primary documents we use to verify them for a loan application.

| Income Source | Primary Documentation Required | Key Consideration for Lenders |

|---|---|---|

| Self-Employed / 1099 | 2 years of tax returns (personal & business), Profit & Loss statements, bank statements. | Lenders look for a stable or increasing trend in net income after expenses, not just gross revenue. |

| Rental Income | Lease agreements, tax returns (Schedule E), and proof of recent rental receipts. | Consistency of occupancy and a clear history of payments are crucial. Future rent is often discounted. |

| Commissions & Bonuses | 2-year history of W-2s or 1099s showing commission/bonus amounts, year-to-date pay stubs. | The lender needs to see that this income is a regular, predictable part of your compensation. |

| Alimony / Child Support | Divorce decree or court order, plus proof of consistent receipt for at least 6-12 months. | The key is proving the payments are stable and likely to continue for at least 3 more years. |

| Asset-Based Income | Statements from retirement accounts (401k, IRA), investment portfolios, or trust funds. | We use formulas to calculate a qualifying monthly income stream based on your total assets. |

This table isn't exhaustive, but it shows that for every type of unique income, there's a clear path to documentation. By providing the right paperwork, you help us build the strongest possible case for your mortgage approval.

How RAC Mortgage Approves Non-Traditional Income

So, how does a lender that understands the modern workforce actually get a loan across the finish line? Here at RAC Mortgage, we look past the limits of a simple W-2 to see the real story behind your financial health. Where some lenders see a roadblock, we see a chance to use different kinds of documents to tell your complete story.

This is where the power of a bank statement loan really shines. We dive deep into 12 to 24 months of your business or personal bank deposits to map out a consistent, reliable cash flow. This approach proves you have a stable income, even if it doesn't show up in a neat bi-weekly paycheck.

By focusing on actual cash flow instead of just what's left after tax write-offs, we build a mortgage application that reflects the true success of your business or freelance work.

Building Your Complete Financial Profile

Bank statements are a great starting point, but they're just one piece of the puzzle. We work to build out a complete financial profile with documents that actually make sense for your situation. It's this flexible, common-sense approach that really sets a dedicated Tampa mortgage lender for unique income apart from the big, traditional banks.

To properly vet different income streams, RAC Mortgage has strong processes, including thorough lead qualification. We typically use a combination of the following to build your case:

- 1099 Forms: We'll look at your 1099s from the past two years to show a solid history of contract work and consistent earnings.

- Profit & Loss (P&L) Statements: A clear, well-organized P&L is a powerful tool. It demonstrates your business's profitability and how you manage your finances.

- Detailed Financial Analysis: Our underwriting team are experts at connecting the dots. They take all these documents and weave them into a clear, compelling story about your earning power.

This custom-fit process is where our expertise with complex financial situations comes into play. If you want to learn more about our flexible lending options, check out our guide on Non-QM loan requirements to see exactly how we can help.

Getting Your Mortgage Application Ready for a Win

Building a strong mortgage application isn't something you do overnight—it starts long before you even fill out the first form. This is especially true if you have a unique income situation. Think of it like a pre-flight check before you take off; you want to make sure every single part of your financial story is clear, organized, and ready for the lender to review.

A winning application tells a simple, clear story of consistent earnings and smart financial decisions. For a Tampa mortgage lender for unique income, seeing that reliable pattern is everything. The first step? Get your documents together way ahead of time.

The real goal here is to hand the underwriter a clean, easy-to-follow financial history. When you remove the guesswork for them, the whole approval process becomes smoother and a lot less stressful for you.

Your Pre-Application Checklist

To put your best foot forward, focus on getting your records in order and keeping your finances tidy in the months leading up to your application. Taking this proactive approach shows lenders you’re a serious, well-prepared borrower.

Here’s a practical checklist to get you on the right track:

- Round Up Your Records: Grab at least two full years of your federal tax returns (both personal and business, if that applies). You'll also want your most recent 12-24 months of bank statements for every personal and business account. Having all this ready from the start prevents frustrating delays later on.

- Whip Up a Clear P&L Statement: If you own a business, a detailed Profit and Loss (P&L) statement is non-negotiable. This document needs to clearly lay out your revenue, expenses, and net profit, giving the lender a quick snapshot of your business's financial health.

- Keep Your Finances Clean: For at least three to six months before you apply, steer clear of making large, undocumented cash deposits. Lenders have to source every dollar, and mysterious deposits can throw up red flags and really complicate the verification process.

By taking these steps, you’re building a foundation of trust and transparency right from the get-go. If you want a more detailed breakdown of all the paperwork you might need, check out our guide on the documents needed for a mortgage application to make sure you haven’t missed a thing.

Here at RAC Mortgage, we know that a well-prepared borrower is an empowered borrower.

Gaining an Edge in Tampa's Housing Market

In a hot market like Tampa, a strong pre-approval isn't just nice to have—it's your secret weapon. It’s more than a piece of paper; it’s a clear signal to sellers that you're a serious buyer who can actually close the deal.

When you're working with unique income, that signal becomes absolutely critical.

Partnering with a specialist like Residential Acceptance Corporation (RAC Mortgage) gives you a real advantage. When sellers see a pre-approval letter from us, they know your unique income streams have already been thoroughly vetted. This isn't some back-of-the-napkin estimate; it's solid proof of your buying power.

A pre-approval from a lender who specializes in non-traditional income tells sellers that the most complex part of your financial verification is already complete, making your offer much stronger.

Competing With Confidence

That confidence can make or break your chances. With forecasts predicting a 1.4% rise in Tampa Bay home prices, the market is only getting tighter. This pressure often leads to stricter underwriting standards, making it even tougher for borrowers with unconventional income to get a standard approval.

A rock-solid pre-approval from RAC Mortgage helps you cut through the noise. It puts you on equal footing with traditional W-2 buyers, proving your offer is just as solid—if not more so. Why? Because the hardest part, the income verification, is already done.

This lets you move fast and negotiate from a position of strength. To see exactly how we pull this off, check out our specialized solutions for a bank statement mortgage in Tampa.

Answering Your Top Questions About Unique Income Mortgages

When you don't have a standard W-2, stepping into the mortgage process can feel like you're navigating a maze. It’s only natural to have a ton of questions. As a top Tampa mortgage lender for unique income, we at Residential Acceptance Corporation (RAC Mortgage) are all about giving you straight answers so you can move forward with total confidence.

Let's dive into some of the most common questions we get from borrowers just like you.

How Many Months of Bank Statements Will I Need?

This is usually the first thing people ask. For a bank statement loan, we’re typically looking at 12 to 24 months of your personal or business bank statements.

Why so many? This long-term view helps our underwriting team see a clear and consistent income pattern, even if your cash flow has its ups and downs from month to month. The exact number of statements we need really depends on your specific financial picture, but our loan officers will work with you to figure out what documentation tells your story best.

Can I Still Get a Mortgage if I Just Became Self-Employed?

While the industry loves to see a two-year track record, we know that’s not everyone's reality. At RAC Mortgage, we get that every business journey is different, and a two-year history isn't a hard-and-fast rule for us.

Maybe you've been self-employed for less than two years but you have a ton of experience in the same field. Or perhaps you have a rock-solid business plan and plenty of cash reserves. In cases like these, we can often build a really compelling application. The best first step is always to chat with one of our specialists about your unique situation.

What's the Minimum Credit Score I Need?

There’s no single magic number here. The minimum credit score for a unique income loan isn't set in stone because it depends on a few moving parts:

- The type of loan program you’re aiming for

- How much you’re putting down

- Your overall financial health and history

At RAC Mortgage, we believe in looking at the whole person, not just a single score. A higher credit score always helps, of course, but our flexible programs are built to work with a wide range of credit profiles. The only way to know for sure where you stand is to connect with us for a personalized look.

Are Interest Rates Higher for These Kinds of Loans?

It's true that interest rates for non-traditional mortgages, like our bank statement programs, can sometimes be a touch higher than a standard W-2 loan. This isn't arbitrary—it reflects the more detailed underwriting and the different kind of risk involved.

That said, RAC Mortgage is committed to fighting for competitive rates by doing a deep dive to document your complete financial strength. Things like a larger down payment or a strong credit score can also help you lock in a better rate. We promise to be completely transparent, giving you a crystal-clear breakdown of every cost and rate tied to your loan.

Ready to see how your unique income can get you the keys to your dream home in Tampa? The team at Residential Acceptance Corporation has the expertise to guide you every step of the way.

Get Your Personalized Mortgage Consultation Today