So, you're ready to figure out what your mortgage payment will actually look like. This is one of the first real steps toward owning a home in Tampa, and honestly, it’s not as complicated as most people think.

It all boils down to four key parts, something we in the industry call PITI: Principal, Interest, Taxes, and Insurance. Here at RAC Mortgage, we've found that walking Tampa homebuyers through this from the get-go gives them the confidence they need to tackle the homebuying process head-on.

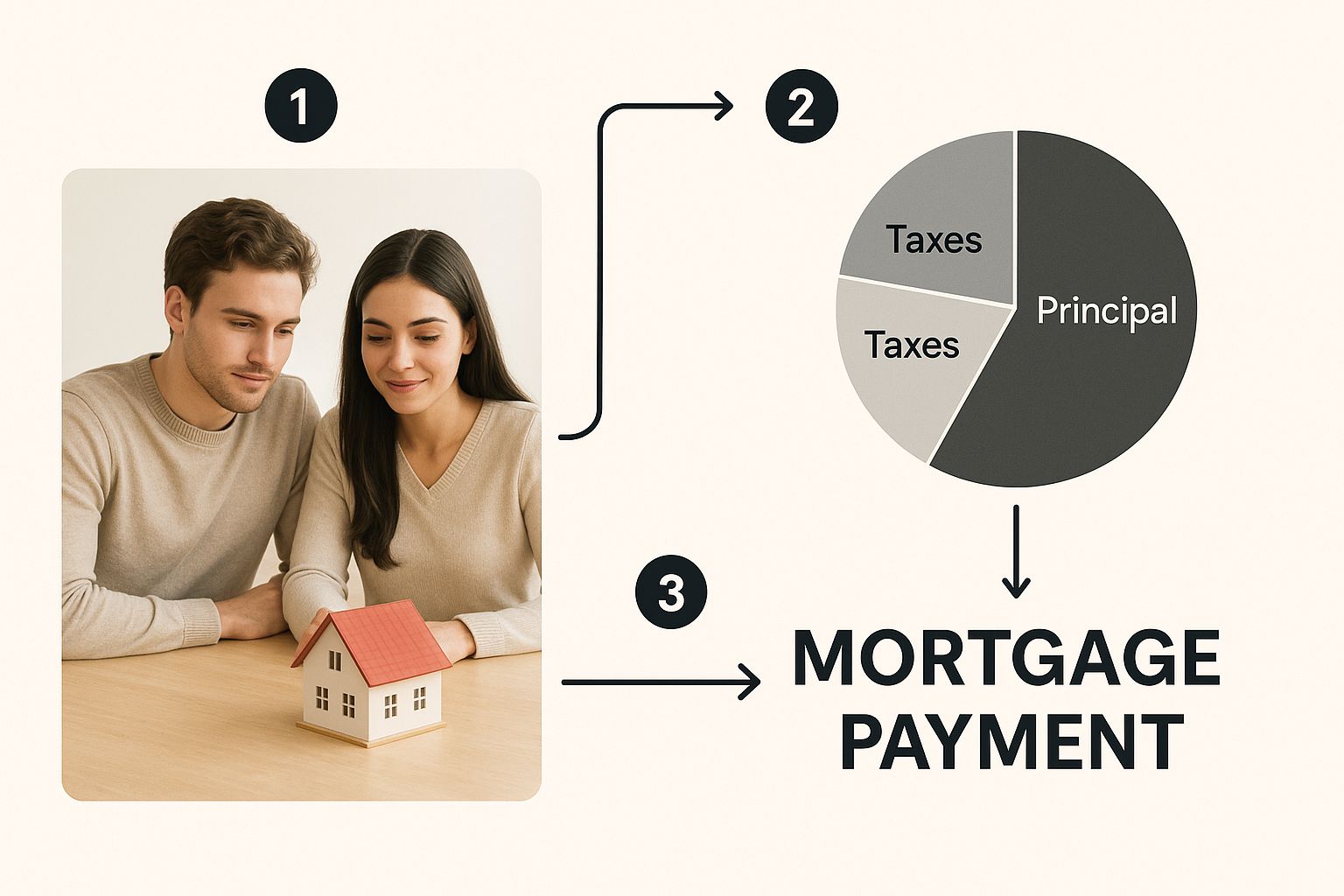

Your Mortgage Payment Explained

Looking at a future mortgage payment is about more than just the home's price tag. It’s a mix of paying back the loan itself and covering all the other costs that come with owning a home. Getting a handle on these components is crucial if you want to build a realistic budget and avoid any nasty surprises later.

The actual math is built on a financial concept called amortization. In simple terms, the amortization formula takes your total loan amount, adds all the interest you'll pay over the years, and spreads it out over a set number of months. The formula juggles the principal, the interest rate, and the loan term.

A typical 30-year fixed-rate mortgage in the U.S., for instance, might have an interest rate around 6.4% APR as of mid-2025. Your payments are structured based on that. If you're curious, you can discover more insights about the amortization formula and how it’s used in modern lending.

The Four Pillars of Your Payment

Your total monthly housing cost is built on these four pillars. Lenders usually bundle them into one single payment for convenience.

- Principal: This is the money you actually borrow from a lender like RAC Mortgage to buy the house. A piece of every payment you make goes toward chipping away at this balance.

- Interest: This is simply the fee for borrowing the principal. A bigger chunk of your early payments goes to interest, but that slowly shifts as you pay down your loan—more and more of your money starts hitting the principal.

- Taxes: These are the property taxes your local government (like Hillsborough County) charges. Your lender will typically collect 1/12th of your estimated annual tax bill each month and stash it in an escrow account to pay for you.

- Insurance: This is your homeowner's insurance premium, which is non-negotiable. It protects your property from damage. Just like with taxes, a portion of this is collected monthly and paid from your escrow account.

Let's break that down even further.

Breaking Down Your Monthly Mortgage Payment (PITI)

This table unpacks the four main parts of a typical mortgage payment to help you understand exactly where your money is going each month.

| Component | What It Covers | Impact on Your Payment |

|---|---|---|

| Principal | The amount you borrowed to buy the home. | Decreases with every payment you make. |

| Interest | The cost of borrowing the money. | Highest at the start of the loan, then gradually decreases. |

| Taxes | Local property taxes for schools, roads, etc. | Can change annually based on property value assessments. |

| Insurance | Homeowner's insurance to cover damages. | Can fluctuate based on your coverage and provider rates. |

As you can see, your payment is a carefully balanced mix of paying back the loan and covering the essential, ongoing costs of homeownership.

This infographic gives a great visual of how these four components all come together.

It really is a blend of paying down your debt while staying on top of the other necessary homeownership costs.

Making Sense of the Mortgage Formula

That long string of letters and numbers, M = P[r(1+r)^n]/[(1+r)^n -1], probably looks like something you’d rather forget from high school algebra. But it’s the engine that powers every single mortgage payment calculation. Think of it as the recipe lenders like us at RAC Mortgage use to figure out what you’ll owe each month.

Once you break it down, it’s not nearly as intimidating as it looks.

At its core, the formula is just a way to balance the money you borrow against the cost of borrowing it over time. Let's translate those variables into plain English so you know exactly what you’re looking at.

The Key Ingredients of Your Payment

Every letter in that formula is a crucial piece of your home loan puzzle. Getting a handle on them is the first step to taking real control of your finances.

- M is for Monthly Payment: This is the big one—the final number you're trying to find. It's the amount you'll pay back each month for the principal and interest portion of your loan.

- P is for Principal: This is simply the total amount of money you borrow to buy your home in Tampa after you've made your down payment.

- r is for Monthly Interest Rate: This is where folks often trip up. Lenders quote you an annual interest rate, but the formula needs the monthly rate. You get this by dividing your annual rate by 12.

- n is for Number of Payments: This one’s straightforward. It's the total number of payments you'll make over the entire life of the loan. For a typical 30-year mortgage, that’s 360 (30 years x 12 months).

The most common point of confusion is easily the interest rate, 'r'. If you have a 6% annual rate, you don't just plug "6" or even "0.06" into the formula. You have to divide that 0.06 by 12 first, which gives you 0.005. It seems like a small step, but it's absolutely vital for an accurate calculation.

The real power of this formula is seeing firsthand how even tiny changes to the principal, interest rate, or loan term can dramatically change your monthly payment and the total interest you’ll pay over decades.

Beyond just your monthly payment, it's also smart for investors to understand how to calculate debt service coverage ratio, which is a key metric for figuring out if a property's income can cover its mortgage.

This formula gives you the Principal and Interest (P&I) part of your payment. Just remember, your total monthly housing cost will also include property taxes and homeowners insurance (often called PITI).

Mastering this core calculation, though, gives you a rock-solid foundation for understanding your entire loan. It also helps you appreciate how other pieces fit together, like how your down payment impacts everything. We dive deeper into that in our guide to the loan-to-value ratio explained. When you understand these elements, you're not just a borrower—you’re a well-informed homeowner.

A Real-World Tampa Mortgage Calculation

Let’s get out of the weeds of pure theory and see how this all plays out in the real world—right here in Tampa. Generic online calculators are a dime a dozen, but they almost always miss the local details that can completely change your monthly payment.

This is where having a Tampa-based pro from Residential Acceptance Corporation (RAC Mortgage) in your corner makes a world of difference.

Imagine you’ve found the perfect spot in a great Tampa neighborhood, maybe somewhere like Seminole Heights or South Tampa. Home prices are always shifting, but we'll use a realistic number to break down how it all works.

Setting the Scene in Tampa Bay

Let’s say the home has a purchase price of $400,000. You've been saving up and are ready with a 10% down payment, which comes out to $40,000. That leaves you with a principal loan amount (our 'P') of $360,000.

Now, for the loan itself. You lock in a 30-year fixed-rate mortgage with an annual interest rate of 6.5%. To get our monthly rate ('r'), we divide 0.065 by 12, giving us 0.005417. Since it's a 30-year loan, the total number of payments ('n') is a nice, round 360.

When you plug all of that into the formula, you get a monthly principal and interest (P&I) payment of about $2,275.

But hold on. That $2,275 is just the starting line. It's only half the story. To budget properly, you absolutely have to account for local taxes and insurance—the 'T' and 'I' in PITI.

Adding Local Taxes and Insurance

This is exactly where local knowledge becomes non-negotiable. A generic calculator might plug in some national average for property taxes, but Hillsborough County plays by its own rules.

- Hillsborough County Property Taxes: The average rate around here is roughly 1.2% of the home's assessed value each year. On our $400,000 home, that's $4,800 a year, or $400 per month.

- Florida Homeowner's Insurance: Let's be honest, Florida's insurance market is its own beast, mostly thanks to our weather. A fair estimate for a home at this price point could be $4,200 annually, which is $350 per month.

Once you add these local costs to your P&I, the real picture of your monthly obligation starts to come into focus.

Your True Tampa PITI Payment

Let’s pull it all together for the full PITI estimate:

| Component | Monthly Cost |

|---|---|

| Principal & Interest (P&I) | $2,275 |

| Estimated Property Taxes (T) | $400 |

| Estimated Home Insurance (I) | $350 |

| Total Estimated PITI | $3,025 |

See that? The gap between the basic P&I and the full PITI is $750 every single month. That's a huge difference, and it’s precisely why a detailed, localized approach is so critical.

By understanding every piece of the puzzle, from the core math to specific Tampa-area costs, you can build a budget that actually reflects reality. The team here at RAC Mortgage specializes in creating these hyper-local calculations to make sure our clients walk into homeownership with their eyes wide open.

Don't Get Blindsided by Costs Beyond Your PITI

Your principal, interest, taxes, and insurance (PITI) payment is the core of your monthly mortgage, but it’s rarely the whole story. To get a real-world number for your budget, you have to look past those four items. Ignoring the other costs that can—and often do—get tacked on is a surefire way to find yourself under financial stress right after moving in.

One of the most frequent additions is Private Mortgage Insurance (PMI). If you put down less than 20% of the home's price, Residential Acceptance Corporation will almost always require PMI. This isn't for your protection; it protects the lender if you can't make your payments. The cost just gets rolled right into your monthly bill, pushing your total payment higher.

Extra Expenses to Watch For in Tampa

Beyond PMI, you’ll find that many Tampa communities have their own recurring fees that are just as mandatory as your mortgage payment. Forgetting to factor these in can completely derail your budget.

- Homeowners Association (HOA) Fees: If you're looking at a condo or a home in a planned neighborhood in the Tampa area, you can bet there’s an HOA. These fees pay for shared amenities like pools, landscaping, and security, and can run anywhere from a modest monthly sum to several hundred dollars.

- Community Development District (CDD) Fees: CDDs are common in newer developments, created to finance the community’s infrastructure—think roads, sewers, and utilities. While they often show up on your property tax bill, they are a separate cost you absolutely need to plan for.

Getting caught off guard by these extra fees is a miserable way to start homeownership. This is where a good loan officer proves their worth. Your RAC Mortgage pro can help you hunt down solid estimates for these costs early on, making sure your final payment calculation is actually accurate.

It's interesting to think about how much things have changed. Before the 1930s, mortgages in the U.S. were a different beast entirely—often short-term, with balloon payments and huge down payments. The long-term, fixed-rate loans we see today have made owning a home possible for more people, but they've also brought a more complex list of potential costs to the table.

Keep in mind, these ongoing expenses are completely separate from your closing costs, which you pay once when you finalize the loan. If you're curious about those upfront fees, our guide covers whether closing costs can be rolled into your loan. Building a true picture of every single fee is the only way to ensure a smooth and stress-free life as a homeowner.

How Your Interest Rate Changes Everything

When you're figuring out how to calculate mortgage payment numbers, you quickly learn the interest rate isn't just another number. It's the king of the board—the single most powerful variable in the whole formula.

A difference of a quarter or half a percent might sound tiny, but it can balloon into tens of thousands of dollars over the life of your loan. This one factor has more sway over your monthly budget and long-term financial health than almost anything else.

Nailing down a lower rate means you pay less to borrow money. Simple as that. It directly shrinks the "Interest" part of your PITI payment, which means more cash in your pocket and faster equity growth. That’s why working with a local Tampa expert like Residential Acceptance Corporation (RAC Mortgage) is so crucial. We know this market inside and out and can track down the most competitive rates for your specific situation.

The Power of a Percentage Point

Let’s put this in real-world Tampa terms. Imagine you're eyeing that same $400,000 home and taking out a $360,000 loan on a 30-year term.

Look at how just one percentage point completely changes the game for your monthly payment and total interest.

| Interest Rate | Monthly P&I Payment | Total Interest Paid (30 Years) |

|---|---|---|

| 6.0% | $2,158 | $416,997 |

| 7.0% | $2,395 | $502,109 |

That single percent jump costs you an extra $237 every single month. Over 30 years? That adds up to a staggering $85,112 in extra interest. That’s money that could have been a college fund, a major home renovation, or a serious boost to your retirement savings.

Factors That Shape Your Interest Rate

Your interest rate isn’t pulled out of a hat. It’s a calculated number based on your personal finances and what’s happening in the broader economy. If you know what lenders are looking for, you can put your best foot forward.

Here are the key things that influence your rate:

- Your Credit Score: This is the big one. It’s a snapshot of your financial reliability, and a higher score almost always means a lower rate.

- Down Payment Amount: Putting more money down reduces the lender’s risk. They often reward that with a better interest rate.

- Loan Type: Different loan programs, like FHA, VA, or Conventional, all have their own rate structures.

- Market Conditions: The health of the national—and even global—economy plays a huge role in where mortgage rates are heading.

A mortgage in Sweden with a 2.84% rate would have a much lower payment than the same loan in the U.S. at 6.39%, showing how much location and economic climate matter. Learn more about how global mortgage rates compare on cepr.org.

When you work with a dedicated loan officer at RAC Mortgage here in Tampa, you have a guide to help you navigate all these factors. We look at your whole financial picture to match you with the best possible loan terms, turning a complicated process into a clear path to owning your home.

Common Questions About Mortgage Calculations

When you're jumping into the Tampa home-buying process, it's completely normal for questions to bubble up, especially around all the math. Getting clear, simple answers is the key to moving forward with confidence.

Here are a few of the most common questions we hear from homebuyers at Residential Acceptance Corporation when they're trying to figure out how to calculate mortgage payment numbers. Our job is to demystify all of this so you can get back to the fun part—finding your perfect home.

P&I Versus PITI

One of the first things that trips people up is the difference between P&I and PITI. It sounds like alphabet soup, but it's pretty straightforward.

P&I is short for Principal and Interest. This chunk of your payment is what actually pays down your loan balance (the principal) and covers the cost of borrowing the money (the interest). Think of it as the core of your loan repayment.

But PITI adds Taxes and Insurance to that core payment. This number gives you the real-world, total monthly cost of your housing. Lenders will usually collect the 'T' and 'I' from you each month, stick it in an escrow account, and then pay your property tax and insurance bills for you when they're due. At RAC Mortgage, we always focus on the PITI estimate to give our Tampa clients the most complete and realistic financial picture possible.

How a Bigger Down Payment Changes Your Calculation

Coming to the table with a larger down payment has a powerful, one-two punch effect on your monthly mortgage payment.

First, it directly shrinks your principal loan amount (the 'P' in the formula). You're simply borrowing less money, which means a smaller monthly payment right out of the gate and way less interest paid over the life of the loan.

The second major benefit is avoiding Private Mortgage Insurance (PMI). If you can put down 20% or more, you get to skip this extra monthly fee entirely. That can save you a pretty significant chunk of change each month. So, a bigger down payment doesn't just cut your main payment—it helps you dodge a whole other cost.

Does This Calculation Work for an ARM?

Yes, this formula is perfect for figuring out the payment during the initial fixed-rate period of an Adjustable-Rate Mortgage (ARM).

Once that introductory period is over, however, the interest rate can adjust based on market conditions, which will change your monthly payment. Calculating those future payments gets tricky because it depends on the ARM's specific terms, caps, and the index it's tied to.

For a clear look at how an ARM might play out over time, it’s best to talk with one of our loan officers. We can model different scenarios for you. A lender's ability to factor in your personal financial health is also important. If you want to see how lenders view your overall financial obligations, you can learn more about the debt-to-income ratio in our detailed guide.

Why Not Just Use a Generic Online Calculator?

Look, those online calculators are great for a quick, back-of-the-napkin estimate. But they almost always miss the crucial local details that can make a huge difference. This is where working with a Tampa-based lender like RAC Mortgage really pays off.

We use current Hillsborough County property tax rates and realistic Florida homeowner's insurance estimates—which can be a lot higher than the national averages those generic calculators use. We also know the typical HOA fees you'll find in local communities. This expertise turns a wild guess into a reliable, personalized calculation you can actually build your budget around.

Ready to get a clear, accurate mortgage payment calculation tailored to your Tampa home search? The experts at Residential Acceptance Corporation are here to provide the local insight and personalized guidance you need.

Get Started with Your Free Rate Quote Today