For countless homebuyers in Tampa, the dream of owning a home feels just out of reach because of traditional lending rules. This is where an unconventional mortgage can be a game-changer, opening doors that a standard loan would keep firmly shut.

So, What Exactly Is an Unconventional Mortgage?

Think of it like this: a conventional mortgage is like buying a suit right off the rack. It fits most people, but not everyone perfectly. An unconventional mortgage, on the other hand, is like getting a suit custom-made by a tailor. It’s designed from the ground up to fit your specific financial situation, especially if you don't have a simple W-2 job.

You'll often hear these loans called non-qualified mortgages (or non-QM loans). That term just means they don't have to follow the very rigid rules set by government-backed entities. But don’t let the "non-qualified" label fool you. It doesn't mean the loan is bad or risky; it simply means it’s different.

Why a Flexible Approach Makes Sense in Tampa

Tampa’s economy is booming, and it’s not just from traditional 9-to-5 jobs. Our city is a hotbed for entrepreneurs, real estate investors, and a whole army of gig economy workers. These people often have strong, reliable incomes, but proving it with pay stubs and tax returns can be a nightmare.

For these hardworking individuals, an unconventional mortgage in Tampa isn't just another option—it's often the only pathway to buying a home. It's a lending solution built on the common-sense idea that financial health isn't one-size-fits-all.

Here at Residential Acceptance Corporation (RAC Mortgage), this is our specialty. We believe a non-traditional career shouldn't lock you out of the housing market, and we're experts at building financing solutions that reflect that.

Who Is This For? A Closer Look

This kind of flexible financing is a perfect match for a growing number of people in our community. An unconventional mortgage could be exactly what you need if you're:

- Self-Employed: Think business owners, freelancers, and independent contractors. We can often use bank statements to show your true income instead of just relying on tax returns.

- A Real Estate Investor: Need a loan based on a property's potential rental income, not just your personal salary? This is the way to do it.

- A Gig Economy Worker: Your income might swing month-to-month as a driver, creative, or consultant. A non-QM loan can account for that.

- Someone with a Unique Situation: Maybe you've had a recent credit hiccup, have a high net worth but low taxable income, or you're a foreign national looking to invest in Tampa real estate.

In short, these loans fill a crucial gap. They serve creditworthy borrowers who are unfairly shut out by automated, box-checking systems. An unconventional mortgage allows a lender like RAC Mortgage to take a holistic look at your finances, making homeownership a reality for more people in Tampa.

Exploring Different Types of Unconventional Loans

Once you realize that a mortgage doesn't have to be a one-size-fits-all product, a whole new world of homeownership opens up. With an unconventional mortgage, the goal isn't to squeeze your finances into a rigid box. Instead, it's about finding a loan that truly reflects your ability to buy a home. Here at Residential Acceptance Corporation (RAC Mortgage), we specialize in these powerful, flexible solutions.

Let's cut through the financial jargon and explore the most common types of unconventional loans by looking at real-world scenarios right here in Tampa. These aren't just abstract financial instruments; they're practical tools built for today's homebuyers.

Bank Statement Loans for Tampa's Entrepreneurs

Picture a successful food truck owner in Ybor City. Business is booming, and cash flow is strong every month, but her tax returns don't tell the full story. After writing off legitimate business expenses—ingredients, staff wages, permits—her documented net income looks much lower than what she actually earns. For a traditional lender, that's a deal-breaker.

This is where a Bank Statement Loan steps in as the perfect solution.

Instead of just looking at W-2s or tax returns, this program lets lenders verify income by analyzing bank deposits over 12 to 24 months. It paints a much more accurate picture of a business owner's real financial situation. For our food truck entrepreneur, her consistent deposits prove she has a stable income that can easily support a mortgage payment.

A Bank Statement Loan is built on a simple premise: your cash flow is your story. It allows self-employed individuals and gig workers in Tampa to qualify for a mortgage based on the actual revenue their business generates, not just what’s left after deductions.

This type of loan is a lifeline for the consultants, freelancers, and small business owners who are the backbone of our local economy. To find out if your business's cash flow could get you into a new home, you can learn more about the specifics of a bank statement mortgage in Tampa.

Investor Cash Flow (DSCR) Loans for Real Estate Investors

Now, think about a real estate investor who wants to buy a rental property near the University of South Florida (USF). They already own a few properties, making their personal tax returns pretty complex. A traditional loan approval process would fixate on their personal debt-to-income ratio and likely turn them down, stopping their portfolio growth in its tracks.

This is exactly the kind of situation where an Investor Cash Flow Loan, often called a DSCR loan, really shines. DSCR stands for Debt-Service Coverage Ratio.

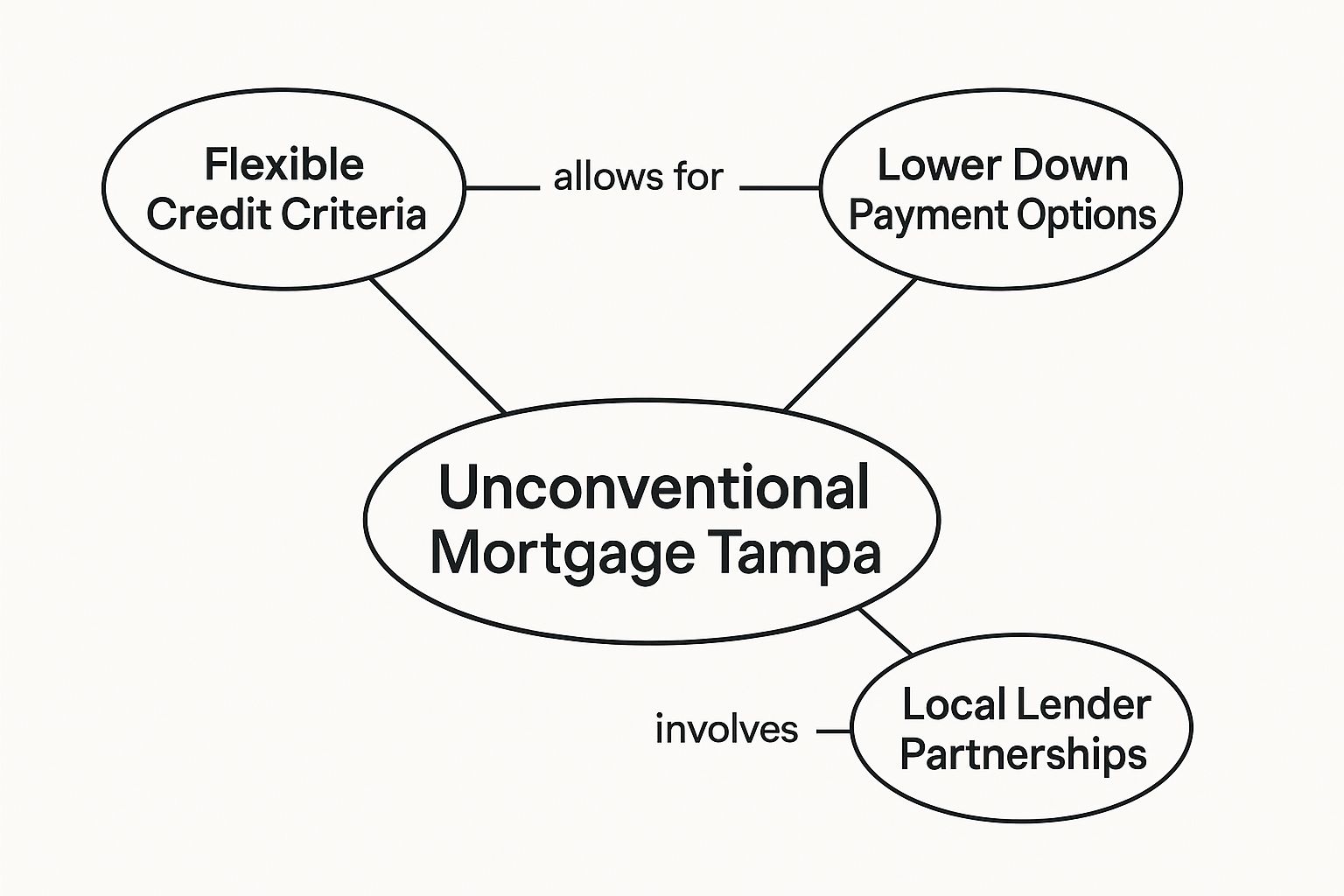

This infographic shows the core benefits that make unconventional mortgages in Tampa so valuable for a wide range of borrowers.

As you can see, the combination of flexible criteria, varied down payment options, and local expertise creates truly powerful financing solutions.

A DSCR loan qualifies the borrower based on the rental property's potential income, not the borrower's personal finances. The lender simply analyzes whether the expected rent will be enough to cover the monthly mortgage payment, taxes, and insurance. If the property's cash flow pencils out, the loan is often approved.

It’s a game-changer for investors.

- No Personal Income Verification: The property’s ability to generate revenue is what matters most.

- Faster Closings: With less personal paperwork needed, these loans can often close much faster—a huge advantage in Tampa’s competitive market.

- Unlimited Properties: Many investors use DSCR loans to scale their portfolios without running into the strict property limits set by conventional lenders.

For the investor looking at that USF rental, this means they can secure the property quickly, using its own income potential to get the financing they need.

Asset-Based Loans for High-Net-Worth Individuals

Finally, let's consider a retiree in a South Tampa condo. She's spent a lifetime building a substantial investment portfolio but has a very low "official" income now that she's no longer working. She wants to buy a second home on the water, but a conventional loan would likely be denied due to her lack of traditional income.

An Asset-Based Loan (or asset-qualifier loan) is the key. This type of loan lets borrowers qualify for a mortgage based on their liquid assets, not their income. Lenders use a formula to calculate a qualifying "income" from the borrower's total assets, proving they have more than enough financial stability to handle the mortgage.

This option is perfect for people who are "asset rich but income poor" on paper. It ensures their wealth is properly recognized and gives them a clear path to financing without needing pay stubs or tax returns. For our South Tampa retiree, it means her years of smart saving and investing can finally help her buy the waterfront home she's always dreamed of.

Who Fits the Bill for These Mortgages?

So, who are these unconventional mortgages actually for? Could one be the key to unlocking your dream home in Tampa? While traditional loans are built for people with a straightforward W-2 and a flawless credit report, the reality is that many successful, financially stable people just don't fit that rigid mold.

That's precisely where an unconventional mortgage in Tampa comes into play. It’s designed for creditworthy borrowers whose financial picture is a bit more complex. Here at Residential Acceptance Corporation (RAC Mortgage), we work with these exact folks every day, helping them leverage their unique financial strengths to buy a home.

The Successful Entrepreneur

Picture the owner of a bustling local business in The Heights. Her company is doing great, but her tax returns are a maze of legitimate write-offs that minimize her taxable income. To a traditional lender's automated system, her income looks too low, and she gets a swift denial, despite having fantastic cash flow.

This is a textbook case for an unconventional loan. By using a bank statement loan, we can look at her business's actual revenue over 12 or 24 months. This proves she has the consistent income to afford the home she wants. Suddenly, her complex finances aren't a roadblock; they're just part of a story we know how to tell.

The Savvy Real Estate Investor

Now, think about a real estate investor trying to snap up another rental property in the hot Seminole Heights market. Traditional lenders get nervous when an investor has too many properties and are obsessed with personal debt-to-income ratios. This can bring an investor's growth to a grinding halt.

The solution? A DSCR (Debt-Service Coverage Ratio) loan.

A DSCR loan flips the script. It focuses on the property’s ability to generate income, not the investor’s personal tax returns. If the projected rent covers the mortgage payment and other expenses, the loan is good to go.

At RAC Mortgage, we use these loans to help investors move quickly in Tampa's competitive market. By letting the property's own potential secure the financing, we empower them to build their portfolios without being held back by outdated rules.

The Gig Economy Professional

Tampa's economy is fueled by gig workers—from freelance creatives in St. Pete to rideshare drivers navigating downtown. These professionals often have income that ebbs and flows from month to month, coming from multiple sources. For a standard underwriting system, this is a major red flag.

An unconventional mortgage, however, is flexible enough to handle this. By looking at a longer history of bank statements or averaging out their income over a full year, we get a much truer picture of their earning power. It’s a common-sense approach that sees a variable income not as a risk, but as a normal feature of their work.

The Foreign National Investor

Tampa’s booming market is catching eyes all over the world. A foreign national who wants to buy a vacation home or a rental property near the water will run into major hurdles with traditional financing. Without a U.S. credit history or income documents, they’re usually out of luck.

This is exactly why specialized non-QM programs were created. These loans for foreign nationals can consider international credit reports, assets held in overseas banks, and other alternative proof of financial strength. This opens the door for international buyers to invest in Tampa real estate, which is great for our local economy.

Considering Tampa's population has grown by 3.3% since 2020 and mortgage payments are often cheaper than rent, the drive to own a piece of this city is strong. You can learn more about Tampa's housing data and demographic trends on graystoneig.com. This makes unconventional financing an essential tool for all kinds of buyers.

Each of these people has a strong financial foundation—it just doesn't look "standard." At RAC Mortgage, we specialize in understanding these unique situations and finding the perfect unconventional mortgage to make their homeownership dreams a reality.

How to Navigate the Application Process

Stepping into the world of an unconventional mortgage in Tampa can feel like you’re entering uncharted territory. But the truth is, the application process is more straightforward than you might expect. With Residential Acceptance Corporation (RAC Mortgage) as your guide, we've designed the journey to be clear and empowering, focusing on your unique financial strengths rather than trying to fit you into a one-size-fits-all box.

The biggest difference comes down to the paperwork. Instead of the usual W-2s and tax returns, this path is all about building a more complete picture of your finances. It’s a common-sense approach, really, because we know that for many successful Tampa residents, true financial health isn't always reflected on a standard tax form.

The Initial Consultation and Pre-Approval

It all starts with a simple conversation. Think of the initial consultation with a RAC Mortgage specialist not as an interrogation, but as a strategy session. We'll sit down and talk about your goals, look at your financial situation, and figure out which unconventional loan program—like a bank statement or DSCR loan—makes the most sense for you.

From there, we work on getting you pre-approved. This involves a preliminary review of your finances to give you a solid idea of how much you can likely borrow. In Tampa's competitive market, a pre-approval letter is a powerful tool. It shows sellers you're a serious, capable buyer ready to make a move.

Gathering Your Alternative Documentation

This is where the path really splits from a conventional loan. Instead of digging up old tax returns, you’ll focus on providing documents that tell the true story of your income and financial stability.

The goal of alternative documentation isn't to hide anything—it's to reveal the full picture. It allows underwriters to see the consistent cash flow or significant assets that traditional paperwork often misses.

The exact documents you'll need will depend on the loan you're getting:

- For Bank Statement Loans: You’ll typically need 12 to 24 months of your business or personal bank statements.

- For DSCR Loans: The focus is on the property's income potential, so we’ll need things like a lease agreement or a rental appraisal.

- For Asset-Based Loans: You will provide statements from your investment accounts, retirement funds, or other liquid assets.

To help you get ready, we've put together a detailed breakdown of the paperwork you might need. You can check out our guide on what documents are needed for a mortgage to get a head start.

Underwriting and Final Approval

Once your file is complete, it heads to underwriting. At RAC Mortgage, our underwriters are experts at looking at non-traditional financial profiles. They know how to look beyond the surface-level numbers to understand the real context of your income or assets, giving your application a fair and thorough evaluation.

A smart move before you even apply is to get a clear picture of your credit history. You can obtain all three credit reports for free to check for any mistakes or inaccuracies ahead of time. Taking this proactive step can save you from surprises during the underwriting phase.

After the underwriter has verified everything and the property appraisal comes in, you'll receive your final loan approval. From that point, it’s a clear path to the closing table, where you’ll sign the final documents and finally get the keys to your new Tampa home. With RAC Mortgage, this entire process is handled with transparency and expertise, making your homeownership dream a smooth reality.

Why Tampa's Market Demands Flexible Financing

Tampa's real estate scene isn't just growing; it's exploding. With strong job growth and a steady stream of people moving here, the market has become incredibly dynamic and competitive. In this kind of environment, speed and flexibility aren't just nice to have—they're essential for getting a deal done.

When home prices are on the rise and bidding wars are common, every dollar and every day counts. The ability to walk in with a strong, confident offer can be the deciding factor. This is where standard, cookie-cutter loans often miss the mark, and why the unique pulse of Tampa’s economy demands a more creative approach to financing a home.

Gaining a Competitive Edge in a Hot Market

For a lot of hopeful buyers, an unconventional mortgage in Tampa is the key that opens doors that would otherwise be locked. It provides the strategic advantage needed to go head-to-head with all-cash buyers and those with seemingly perfect financial profiles.

Think about a self-employed business owner who wants to buy in a sought-after neighborhood like South Tampa or Seminole Heights. Their income is fantastic, but their tax returns don't paint the full picture of their cash flow. A bank statement loan from Residential Acceptance Corporation (RAC Mortgage) lets them get a pre-approval that reflects their actual financial health, empowering them to make a competitive offer the moment they find their dream home.

It’s the same story for real estate investors trying to grow their portfolios. They have to move fast.

In a market where a great rental property can attract multiple offers in a matter of days, you can't afford to be held up by a slow, traditional lender. An unconventional loan is often what separates a successful investment from a missed opportunity.

This is where tools like Investor Cash Flow (DSCR) loans really shine. They allow an investor to get financing based on the property's income potential, not their personal W-2s. This completely bypasses the long, drawn-out income verification process, helping them close deals quicker and scale their investments more effectively.

Solving Unique Property Challenges

It’s not just about the competition for single-family homes. Tampa’s market is also full of unique properties, especially condominiums, which come with their own financing headaches that many conventional lenders just aren't prepared for.

For instance, getting a loan for a condo in Florida has become a major challenge. As of March 2025, a surprising number of condo buildings have been flagged as ineligible for conventional loans due to issues with insurance, financial reserves, or deferred maintenance. This has created a sort of "blacklist" that shuts out potential buyers, even for perfectly fine units. You can read more about these condo financing hurdles on tampabay.com.

Here again, an unconventional mortgage offers a vital workaround. With more flexible underwriting standards, these loans create a path to ownership for people who want to buy a condo that doesn't fit into a neat conventional box. For anyone in this situation, it’s worth seeing how a Tampa mortgage lender with flexible guidelines can navigate these tricky scenarios.

Whether you're an entrepreneur, an investor, or someone with your eye on a unique property, the Tampa market requires more than a generic loan. It calls for a financing partner who gets the local scene. With a smart solution from RAC Mortgage, an unconventional loan isn't just an alternative—it's your most powerful tool for winning in this market.

Common Questions About Tampa Unconventional Mortgages

Dipping your toes into the world of non-traditional financing naturally brings up a few questions. That's perfectly normal. Our goal here is to give you straight, clear answers to help you move forward with confidence and bust some common myths about getting an unconventional mortgage in Tampa. Think of this as your personal FAQ, backed by the hands-on experience of Residential Acceptance Corporation (RAC Mortgage).

Are the Interest Rates on These Loans a Lot Higher?

It's a fair question, and the answer is nuanced. While rates for unconventional loans can be slightly higher than for conventional ones, they are still very competitive in today's market. That small difference in rate is what allows for the lender's flexibility—it's what makes it possible to approve a loan based on your unique financial picture.

Think of it this way: the rate is just one part of the overall value. It's the key that unlocks the door to homeownership for many who wouldn't qualify otherwise. Here at RAC Mortgage, our job is to hunt down the most favorable terms for your specific situation, making sure your Tampa mortgage is a smart financial move.

How Long Does It Actually Take to Get Approved?

The timeline for an unconventional mortgage is surprisingly similar to a conventional loan, typically landing somewhere between 30 and 45 days. The real secret to a quick, smooth process is preparation. Having your alternative documentation, like bank statements or asset schedules, organized and ready to go makes all the difference.

Our experienced team at RAC Mortgage will guide you through exactly what's needed, every step of the way. We help you gather the right paperwork to ensure an efficient, on-time closing for your new Tampa home.

A common misconception is that "unconventional" automatically means slower. The truth is, when you work with a specialist like RAC Mortgage who lives and breathes these loans, the process can be incredibly streamlined. We know exactly what underwriters are looking for and how to build a strong case from day one.

Can I Refinance into a Conventional Loan Later?

Yes, absolutely! In fact, many Tampa homebuyers do just that. They use an unconventional mortgage as a smart, strategic tool to get into a home now, especially in a competitive market like ours. It serves as a powerful bridge to more traditional financing down the road.

For instance, a self-employed business owner might use a bank statement loan to buy their dream home today. A couple of years later, with a solid track record of income on their tax returns, they can easily refinance into a conventional mortgage to potentially snag an even lower rate. If that's your goal, RAC Mortgage can help you map out a long-term strategy, advising you on how to best position yourself for a future refinance.

Is a Huge Down Payment Always Necessary?

Not at all. The down payment requirements for unconventional mortgages are much more flexible and really depend on the specific loan program and your overall financial profile.

While certain investment property loans might require 20-30% down, many programs designed for a primary residence offer far more adaptable options. We're not bound by the rigid, one-size-fits-all rules of conventional lending; these solutions are built around you.

At RAC Mortgage, we'll explore different scenarios to find a loan that aligns perfectly with your available funds and your homeownership goals in Tampa. The focus is always on creating a sustainable and affordable path to owning your piece of our vibrant city.

Ready to see how an unconventional mortgage could open the door for you? The team at Residential Acceptance Corporation is here with the expert guidance you need.