For a lot of hopeful homebuyers in Tampa, especially those with a unique financial story, finding the right mortgage can feel like an uphill battle. If you're looking for a Tampa manual underwriting mortgage lender, you've found the right place. Residential Acceptance Corporation (RAC Mortgage) specializes in this exact kind of personalized, common-sense approach to getting you into a home.

Your Path to a Tampa Mortgage with Manual Underwriting

Let's be honest: for many people in Tampa, a standard, cookie-cutter mortgage application just doesn't tell the whole story.

Automated underwriting systems are built on rigid algorithms. They're designed to check boxes, and if your finances don't fit perfectly into those boxes, you often get a quick rejection. This happens all the time to great candidates—especially self-employed folks, gig economy workers, or anyone who has worked hard to overcome a past credit stumble.

Manual underwriting is the solution. It offers a powerful, human-centered alternative.

Think of it less like a rigid calculation and more like a real conversation about your finances. Instead of just feeding numbers into a computer, a human underwriter at RAC Mortgage will personally review your entire file. They take the time to look beyond the raw data to understand the context of your financial life. The whole point is to find reasons to approve your loan, not excuses to deny it.

Why a Human Touch Matters in Tampa

In a hot and competitive market like Tampa's, this kind of personalized review can be the one thing that gets you the keys to your dream home. It allows for a much more holistic look at your actual ability to repay a loan.

Here are the key benefits of having a real person on your side:

- Understanding Complex Income: We know how to properly evaluate the fluctuating income that comes with entrepreneurship or freelance work.

- Overcoming Past Credit Issues: A previous bankruptcy or a blemish on your credit report doesn't have to be a permanent roadblock. We see the person, not just the past event.

- Seeing the Big Picture: We look at "compensating factors" that automated systems completely ignore, like a large down payment, significant savings, or a stable job history.

Of course, a vital first step in securing any home loan is getting familiar with the mortgage pre-approval requirements. Knowing what's needed upfront makes the whole journey smoother, whether you end up needing an automated or a manual review.

The core principle of manual underwriting is simple: your financial history is more than just a credit score. It's a story of responsibility, resilience, and readiness for homeownership.

At RAC Mortgage, we don't just use this philosophy—we champion it. We truly believe that a detailed, human-led review provides a much fairer path to homeownership for so many deserving Tampa residents.

To see how our personalized process can work for you, check out our guide on finding a Tampa mortgage lender with flexible guidelines.

What Manual Underwriting Actually Means for You

Let’s cut through the jargon. Think of a standard, automated mortgage system as a vending machine—it only accepts exact change. If your financial profile has anything slightly out of the ordinary, like a mix of income sources or a slightly beat-up credit history, the machine just rejects it. No questions asked.

Manual underwriting, on the other hand, is like talking to the friendly owner behind the counter. They listen to your story. They understand the nuances. They see the person, not just the transaction. It’s a process built on human logic, not rigid code.

A Human Review of Your Financial Story

Here at Residential Acceptance Corporation (RAC Mortgage), that human element is everything. Instead of feeding your application into an algorithm for a simple yes or no, a real, experienced underwriter sits down with your file. They don't just see numbers; they see your story.

This means they’re looking for patterns of responsibility, not just perfection. Maybe you had a past credit hiccup or your income fluctuates because you run your own business. That doesn't mean an automatic "no." Our team is trained to connect the dots and see the real picture of your ability to afford a home.

They'll actually analyze your bank statements to understand your cash flow, review your P&L statements to see the health of your business, and read your letters of explanation to get the context behind a credit blip. It's a deep-dive evaluation that software simply can't do.

At its heart, manual underwriting is about assessing your actual capacity for homeownership, not just checking boxes on a form. It replaces algorithmic rigidity with human reason and common sense.

Why This Matters in Tampa's Dynamic Economy

This personalized approach is a huge deal in Tampa’s vibrant economy. Our region is a magnet for entrepreneurs, freelancers, and gig workers whose income doesn’t fit into a tidy nine-to-five box. An automated system just doesn't know what to do with that, and it leads to a lot of unfair denials.

This is where finding the right Tampa manual underwriting mortgage lender becomes a game-changer. For borrowers who don't fit the conventional mold, manual underwriting is more than just an alternative—it's often the only path to homeownership. By involving a detailed, human review of your entire financial situation, we can unlock doors for self-employed individuals and those with non-traditional income.

It’s about making the market more inclusive, right here in Tampa's competitive housing scene. You can discover more about how this benefits Tampa borrowers at racmortgage.com.

Is a Manually Underwritten Loan Right for You?

So, who is manual underwriting actually for?

It isn't some secret pass for every borrower, but for many hopeful Tampa homebuyers, it’s the key that finally unlocks the door to homeownership. Think of it as a custom-tailored suit versus one off the rack. It’s a process specifically designed for people whose financial lives don't fit into a neat, automated box.

If you find yourself nodding along with any of the profiles below, a manually underwritten loan could be exactly what you need.

The Successful Entrepreneur or Freelancer

Are you a small business owner, a freelance creative, or a gig economy pro here in Tampa? If so, you already know that your income can be a rollercoaster. One month might be a record-breaker, while the next is slower as you line up new projects. Automated systems see this variability and immediately flag it as a risk.

An experienced Tampa manual underwriting mortgage lender like Residential Acceptance Corporation knows better. We understand the hustle. Our underwriters don't just glance at a single number; they dive into your profit and loss statements and bank records to see the real story of your business's health and cash flow. To get a better feel for this, you can learn more about our bank statement mortgage options in Tampa.

The Borrower Rebuilding Credit

Life happens. A past bankruptcy, a tough foreclosure, or a period where you missed some payments can tank your credit score, leading to an instant "no" from a computer. But a past event doesn't have to define your financial future.

This is where manual underwriting truly shines. It gives you the chance to tell your story. Our team at RAC Mortgage will actually read your letters of explanation and look for the hard work you’ve put into re-establishing good credit. We care more about your recent history of on-time payments and your current ability to manage a mortgage than a mistake from years ago.

With manual underwriting, your financial past is context, not a verdict. We prioritize your current stability and readiness for homeownership.

Borrowers with Unique Financial Profiles

Many other situations just make more sense with a human reviewer. You might be a perfect candidate if you have:

- A Lower Credit Score but a Solid Down Payment: Putting down a substantial amount, like 20% or more, is a powerful statement. It shows you have serious skin in the game.

- Significant Cash Reserves: Having plenty of savings left after closing demonstrates smart financial planning and gives you a crucial safety net.

- Minimal Debt: A low debt-to-income (DTI) ratio is one of the clearest signs you can comfortably handle a new mortgage payment.

This is a totally different way of looking at a borrower's file. Instead of plugging numbers into a rigid formula, a human underwriter connects the dots to see the full picture.

The table below really highlights how differently your profile is viewed when an expert gets involved.

How Automated Systems vs Human Underwriters See Your Application

A side-by-side look at how a rigid algorithm and RAC Mortgage’s hands-on review process evaluate the same borrower.

| Borrower Characteristic | Automated System View | RAC Mortgage Manual Underwriting View |

|---|---|---|

| Fluctuating Income | High Risk: Sees inconsistency and potential instability, often leading to denial. | Context-Driven: Analyzes bank statements and P&L to understand business cycles and true average income. |

| Past Credit Event | Disqualifying: A bankruptcy or foreclosure often triggers an automatic rejection regardless of recent history. | Opportunity for Explanation: Views the event as part of a larger story, focusing on recent credit rebuilding and stability. |

| Low Credit Score | Automatic Rejection: The score is often the primary factor, ignoring other financial strengths. | Holistic Assessment: Considers compensating factors like a large down payment or low DTI to balance the score. |

Ultimately, the goal of manual underwriting isn't to find reasons to say no—it's to find the common-sense path to "yes" for qualified borrowers who just don't fit the standard mold.

A Step-by-Step Look at the Manual Underwriting Process

Walking into the manual underwriting process can feel a bit like heading into uncharted territory. But with a clear map, it’s really just a simple, logical journey. At Residential Acceptance Corporation (RAC Mortgage), we’ve spent years refining our process to be as transparent and supportive as possible, taking the guesswork out of it from day one. It’s all about building your story, one piece at a time.

It all starts with a conversation, not a pile of paperwork. During our initial chat, we’re not just plugging numbers into a calculator; we're listening. We want to hear about your work, your financial journey, and what you’re hoping to achieve with a new home in Tampa. This conversation is the foundation we build everything else on.

From there, we’ll help you pull together the documents needed to bring that financial story to life.

Assembling Your Financial Narrative

Unlike the automated systems that just want a W-2 and a few pay stubs, manual underwriting often needs a bit more detail. This isn't about making you jump through hoops. It’s about gathering the right evidence to build the strongest possible case for your approval, and we’ll explain exactly why each piece of the puzzle is important for your specific situation.

Here are some of the documents we often ask for:

- Bank Statements: Looking at the last 12-24 months gives us a clear picture of your cash flow and financial discipline—something that’s absolutely critical for self-employed borrowers.

- Profit and Loss (P&L) Reports: If you run a business, a solid P&L shows us that it's stable and profitable over time.

- Letters of Explanation (LOX): Life happens. A letter of explanation provides the crucial context behind a past credit hiccup, like a bankruptcy or a late payment, allowing a real person to understand the why behind the what.

- Proof of Alternative Credit: For anyone with a thin credit file, showing a solid history of on-time rent and utility payments can be a powerful way to prove you’re reliable.

Figuring out exactly what paperwork you’ll need is a key step, and our team will give you a detailed checklist. If you want a general idea of what to expect, you can check out our guide on what documents are needed for a mortgage application.

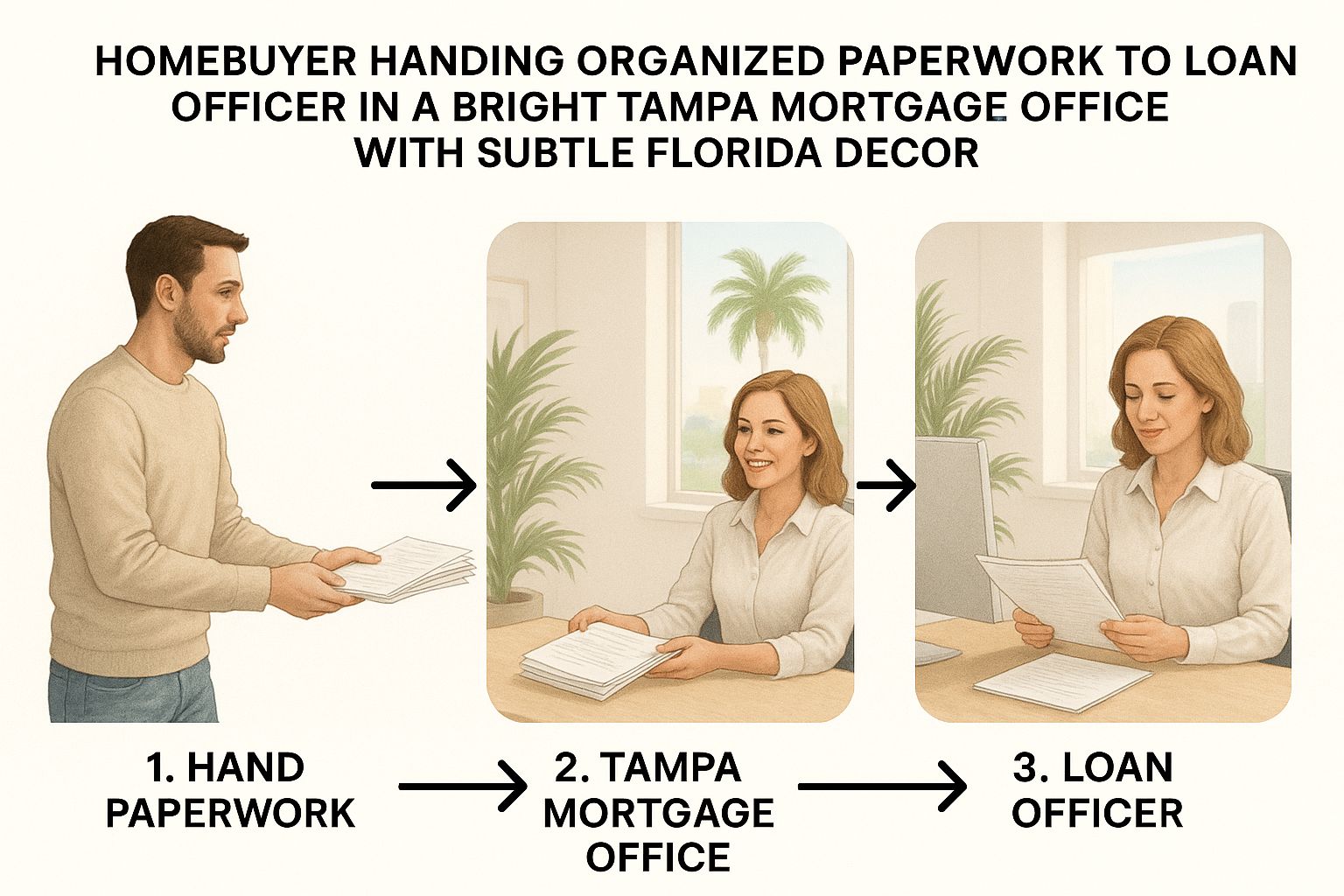

This infographic breaks down the clear, collaborative path from our first conversation to your final loan approval.

As the image shows, getting your documents organized and submitted is a pivotal moment where you and your loan officer team up to build a compelling case.

From Submission to Decision

Once your file is complete, our underwriter dives in for a comprehensive review. This part of the process is all about open communication. We make sure you’re kept in the loop with updates and are here to answer any questions that come up. Think of us as your partners, dedicated to presenting your financial history in the best possible light to get you that final approval you’ve been working toward.

Why RAC Mortgage Is Your Ideal Tampa Lending Partner

Let’s be honest: choosing the right lender in a hot market like Tampa is probably the biggest decision you'll make on your path to owning a home. You need more than a faceless loan processor who just shuffles papers. You need a real partner, someone who gets the local market and is actually invested in seeing you get the keys.

That’s exactly where we, Residential Acceptance Corporation (RAC Mortgage), come in.

We aren't just another company with a menu of mortgage products. We're specialists who live and breathe the Tampa market, and our sweet spot is helping people who don't fit into the traditional lending box. Our whole approach is built on one simple idea: your financial story is unique, and it deserves a thoughtful, human review.

More Than Just Paperwork

Our commitment goes way beyond just pushing an application through a system. We take the time to actually understand your situation, digging deep to find the "compensating factors" that automated underwriting systems are programmed to completely ignore.

Things like a big down payment, a healthy savings account, or a long history of paying your rent on time—these are powerful signs that you’re ready for a mortgage. We make sure those details get the spotlight they deserve.

To make sure we can give our full attention to borrowers who need this hands-on approach, a good lender needs an effective lead qualification process. This helps us identify serious applicants right away and focus our energy on building a rock-solid case for them.

Our reputation is built on one core principle: finding a way to say ‘yes’ when other lenders might say ‘no.’ We’ve helped countless clients who were unfairly shot down by rigid algorithms, turning their frustration into a celebration at the closing table.

Navigating Tampa's Dynamic Market

Being financially resilient is more important than ever, especially in a fast-changing economy. The numbers back this up. Recent data showed that around 5.5% of Tampa Bay home mortgages were 30 or more days past due, a noticeable jump from 3.3% the year before. You can see more on Tampa's mortgage trends on axios.com.

In times like these, our human-first risk assessment provides a reliable path forward. We can look at things like a temporary dip in income or a recent financial recovery—details that automated systems flag as high-risk—and see the bigger picture.

Choosing RAC Mortgage means you're partnering with a Tampa manual underwriting mortgage lender that sees your potential, not just a snapshot of your past. We believe in common-sense lending for the real people who make our community great.

At the end of the day, our goal is simple: to provide a clear, supportive, and successful path to homeownership. We are here to be the lender that listens, understands, and delivers for Tampa's aspiring homeowners.

Common Questions About Manual Underwriting in Tampa

Jumping into the manual underwriting process naturally brings up a few questions. That's perfectly normal. To help you feel more confident and prepared, we've put together some of the most common things we hear from Tampa homebuyers, along with clear answers on how we handle things at Residential Acceptance Corporation (RAC Mortgage).

Our whole goal here is to take the mystery out of it all. We want to show you that a human-first approach is meant to be supportive, not stressful. Let's dig into the details so you know exactly what to expect when you work with a dedicated Tampa manual underwriting mortgage lender.

Is Manual Underwriting Slower Than Automated Underwriting?

This is easily one of the first questions people ask. And it makes sense—you're anxious to get into your new home! While a manual review is definitely more thorough, it doesn't automatically mean it's a painfully slow process. Our underwriters at RAC Mortgage have this down to a science, with a fine-tuned system for gathering and reviewing everything needed to keep your application moving.

Honestly, a complete and well-organized application can sail through our manual process pretty smoothly. The extra day or two it might take for a real person to look over your file is a tiny price to pay for getting a "yes" that an algorithm would have likely shot down in seconds. We're focused on being both thorough and timely.

The real value isn't just speed; it's the quality of the decision. A swift denial from an algorithm is fast but unhelpful. A thoughtful approval from a human underwriter, even if it takes a bit longer, is life-changing.

Will My Interest Rate Be Higher With a Manual Loan?

This is a big misconception we hear all the time. Your interest rate isn't based on how your loan was underwritten; it’s based on your overall risk profile—the complete financial picture you present.

While it’s true that some very complex financial situations might lead to a higher rate, having strong "compensating factors" can help you land some really competitive terms. RAC Mortgage’s underwriters are trained to hunt for these strengths, like a solid down payment or a low debt-to-income ratio, to balance out your file. Our aim is always to find a fair, sustainable rate that actually fits your unique situation.

What Are the Best Compensating Factors to Have?

Think of compensating factors as the gold stars on your application. They're the positive elements that help offset any perceived weak spots, like a credit score that’s seen better days or income that doesn't come from a typical 9-to-5 job. They are the secret sauce of a manual review.

Based on our experience at RAC Mortgage, these are the factors that make the biggest impact:

- A Significant Down Payment: When you put down 20% or more, you’re showing serious commitment. It immediately lowers the lender's risk.

- Ample Cash Reserves: Having several months' worth of mortgage payments still in the bank after you close is a huge sign of smart financial planning.

- A Low Debt-to-Income (DTI) Ratio: This is just a clear, simple signal that you can comfortably manage the new mortgage payment each month.

- Stable Employment or Business History: A long, consistent track record in your line of work proves your income is reliable and not just a fluke.

- Strong Rental History: If you have a history of paying rent on time—especially if that rent payment is similar to or even higher than your new mortgage payment—that's powerful proof you can handle the responsibility.

Can I Get a Manually Underwritten FHA or VA Loan?

Absolutely! In fact, many government-backed loans like FHA and VA loans often require manual underwriting. This is especially true if a borrower's credit score is on the lower side or if there are other unique financial details in the mix.

The team at RAC Mortgage has deep expertise in the manual underwriting guidelines for these specific programs. This allows us to use the unique flexibilities that are built right into the FHA and VA rulebooks—a critical service that opens the door to homeownership for so many deserving veterans, first-time buyers, and families across the Tampa Bay area.

Ready to see if manual underwriting is the right path for you? The team at Residential Acceptance Corporation is here to listen to your story and guide you through every step.

Start Your Homeownership Journey with RAC Mortgage Today